Weekend Analysis

This was an important week in an earning season with a number of heavyweights publishing their earnings. Investors had been anxious in anticipation given the megacaps rally have been supporting the Market this year and rightly worried whether these firm can maintain their gains given gloomy economic outlook. At last the megacaps did not disappoint with robust results from Microsoft Corp. (MSFT) and Google parent Alphabet Inc. (GOOGL) earlier in the week followed by Meta Platforms Inc.'s (META) as the social media giant surpassed Wall Street expectations for earnings and revenue in its quarterly report.

However, the Econ data coming out of the US continues to disappoint. The MAR capital goods new orders nondefense ex-aircraft and parts, a proxy for capital spending, fell -0.4% m/m, weaker than expectations of -0.1% m/m. The US economy in Q1 grew less than expected with reports showing weekly jobless claims unexpectedly fell, and inflation pressures remain elevated as the Q1 core PCE deflator, which is the Fed's preferred inflation gauge, eased to +4.6% y/y from +4.7% y/y in Mar, rose more than expected.

The weekly initial unemployment claims unexpectedly fell by 16k to 230k, showing a stronger labour market, expectations were for an increase to 248k. Weekly continuing claims unexpectedly fell 3k to 1.858 million, showing a stronger labour market than expectations of an increase to 1.870 million.

US MAR pending home sales unexpectedly fell -5.2% m/m, weaker than expectations of an +0.8% m/m increase and the biggest decline in 6 months.

Meanwhile, US GDP numbers showed the economy grew at a softer-than-expected 1.1% annual pace during the Q1'23 against the forecast of a 2% increase. Inflation rose at an annual 4.2% pace in Q1, compared with a 3.7% increase in Q4'22.

In other Econ data for MAR, personal spending was unchanged m/m, stronger than expectations of -0.1% m/m and personal income rose +0.3% m/m, stronger than expectations of +0.2% m/m. The Q1 employment cost index rose +1.2% (q/q annualized), stronger than expectations of +1.1%

Bank issues and concerns about a slowing economy and possible recession remain on the front burner ahead of a Fed policy announcement next week.

The job market and consumer spending have held up remarkably well despite the Fed raising interest rates as high and as fast as they have...but the economy is slowing and inflation is not anywhere near the Fed's target of 2%

So the Fed has been and will remain deliberately slow and eventually will cut rates aggressively, but only when the coincident and contemporaneous indicators they are focusing on begin to roll over. Principally, what they're really waiting for is for a contraction in non-farm payrolls. For them, that is the holy grail. Don't expect this to be a long wait as we're starting to see cracks in the labour market. We are seeing contraction in important, economically sensitive sectors: financials; retailers; manufacturing, and construction. Companies are cutting hours worked. The work week is a leading economic indicator. Non-farm payrolls are a coincident indicator. The unemployment rate is a lagging indicator. The work week is a classic leading barometer because employers tend to cut hours before they cut staff.

Looming over everything though is the continued standoff in the US over extending the debt ceiling, as the bill passed by House Republicans including sweeping spending cuts - it has already been called DOA by top Senate Democrat Chuck Schumer. Another mouthpiece, Ms Raimondo the Secretary of Commerce warned during the week that the Chinese cloud computing companies may pose a national security threat and the outcome, a 1% drop in Hang Sengs' tech sector.

The result was that all three US indexes managed a move up to post Green week with a BuRPI. All three are currently faced with CAT Res above and need a BO of this area to suggest the momentum can be maintained. Nasdaq is slowly creeping its way towards the Bearish floor and its the closest it has been to leaving this zone since it spent one week in the correction area back in AUG22.

S&P closed at its highest monthly close since MAR22 whilst Nasdaq last posted a higher monthly close in JUL22.

The VIX weekly average reversed a five week Bear run thanks to the spike up during the week when it nearly tested the RN20 but has since PB to close at its lowest since 03NOV21. Short selling spiked up to moved in to the top quartile and Stocks above their DVI's dropped a little but remain largely in the same area below its median.

In the UK the FTSE had a poor start to the week which it maintained until Friday when it finally posted a Green bar, however this was not enough for the index to post a Red week and halt a five week Bull run. The index still has the comfort of the d50MA support below. The index fell just 6 points short of its highest monthly close of FEB23.

All four indexes posted a Green month to make it 3 Green months from 4 in 2023.

Cable having threatened the RN1.25 for several weeks finally managed to BO of this zone which was largely achieved on the US open on Friday. As mentioned a few weeks ago, I still want to see this pair move up a little further before retesting the RN supp to continue the move up and in which case the pair will have a clear run to the Res zone of WVI with RN1.30 just above it. On the monthly the pair posted another Green month to now show a move up of 500pips since 01MAR and post its highest monthly close since MAY22. Long term view on this pair remains Bullish and is supported by the w50MA turning Green with upward trajectory.

Both the Bitcoin and Ethereum posted a Green week but remain short of the RN Res and the high achieved earlier this month.

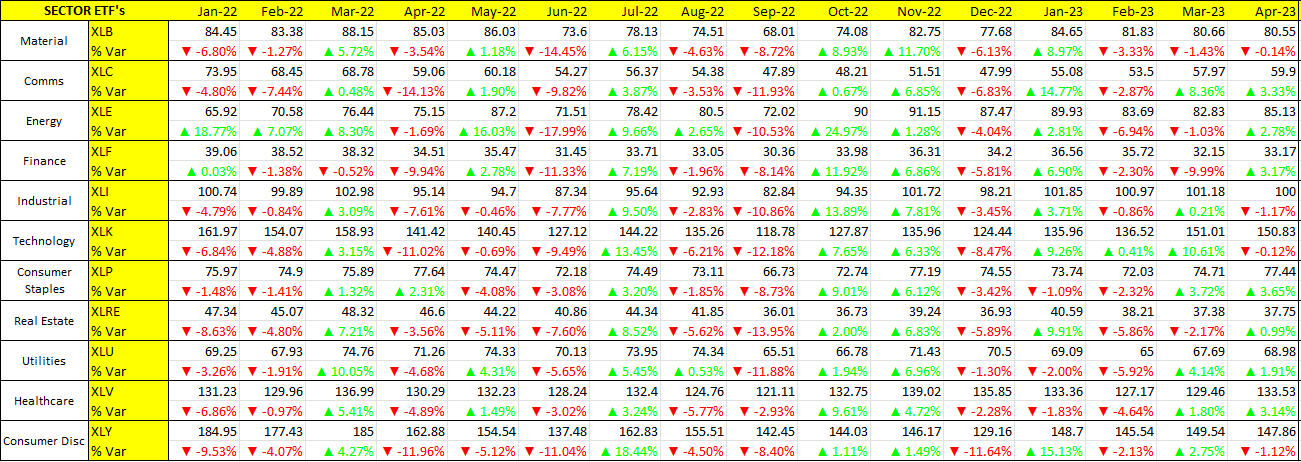

We had another week of mixed performances for the Sector ETF's with a Bullish bias seeing 6 of the sectors posting a Green week led by Communications (XLC) which has now posted 13 Green weeks from 17 this year. Whilst we had 5 Sector ETF's posting a Bearish week, with the exception of Utilities (XLU) which posted a nearly 1% drop, the others were relatively small drops.

Utilities (XLU) and Staples (XLP) remain the Sectors with momentum in the Improving quadrant and of the rest, Healthcare (XLV) remains of interest as its continues its upward momentum to join them.

Communications (XLC) still leads Technology (XLK) and Discretionary (XLY) in the race for the years star performer. Though it is now faced with the WVI/RBN60 Res above. Technology (XLK) has BO of the RN150 and is immediately faced with its dCAT Res.

Finance (XLF) the years ugly duckling has found support at its WVI where it posted a wBuRPI and is fast catching up Energy (XLE) at the rear. Are we soon to see a change in the wooden spoon holder?

Next week we have another busy week on the Econ Data that will culminate in the NFP publication on Friday. We also have Rate decision for USD, AUD and EUR during the week.

May day holiday means major European and UK markets will be closed on Monday.

Enjoy the long holiday Weekend.

Anil Dala

Let's go trade!